I love Fogo de Chao. Love its meat and food~ Let's see if I will love its stock equally :D

1. Adjusted EBITDA is here!

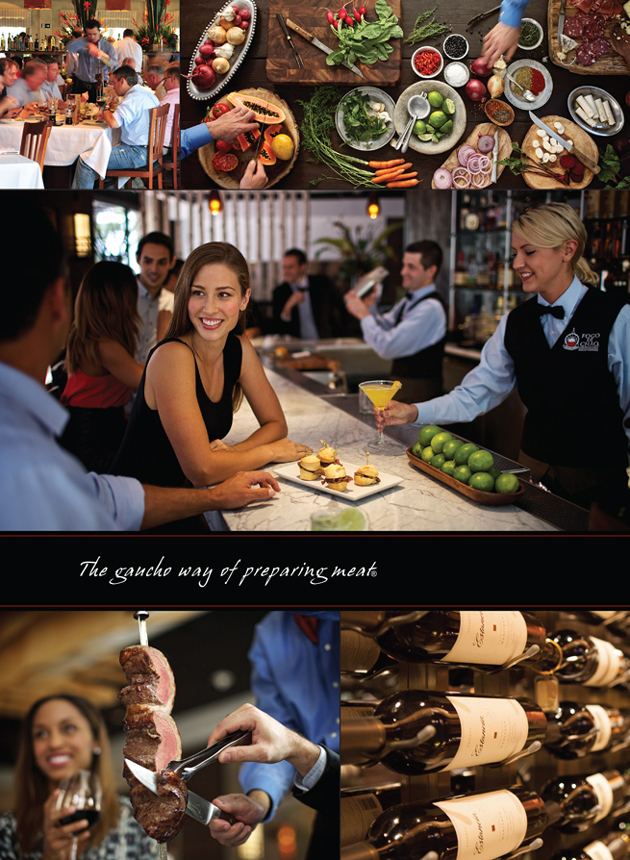

2. Fogo de Chao is 35 years old and features up to 20 cuts of meat.

3. Each restaurant generates 8 million with a gross margin of 32.5%, this is really high.

4. I am not sure if interactive and approachable fine dining experience is the case. Basically, I just tell what meat I want not sure if that is really interactive or approachable.

5. An average person spent $59, yup, this is definitely high end category. On average, a new restaurant recovered 40% of the initial investment within the third year. So within seven years, everything will flow to profits directly, wow.

6. Make more by using bars, alcohol only accounted for 17% of the revenues.

7. Have an expert real estate team so this should be favorable. I am not sure if I can evaluate this though.

8. They decreased food and average cost even when beef price jumped 20%. This is really operation skill :D

9. Anti-takeover...not so lovely governance structure.

10. OK more than half of the assets is goodwill!! hmmm...Has some debt.

11. Restatement of SAR plan...ooohhh not big but still not good.

Assessment.

Pros: High gross margin, strong operating history, and experienced management. Good at managing costs.

Cons: There is restatement, which is never good.

Overall, I think Fogo de Chao may be a good buy given its operational strength. Further, due diligence coming up~

*From Fogo de Chao S-1

No comments:

Post a Comment